March 2026 marked a sharp inflection point for global markets, as escalating geopolitical risks abruptly displaced economic resilience as the dominant driver of asset prices. Unlike prior episodes of volatility, the March drawdown was notable for its scope and speed, as markets shifted quickly from rotation to outright de-risking. The month was dominated by a rare convergence of market-moving events: a severe oil shock stemming from an intensifying conflict involving Iran, a highly anticipated Federal Open Market Committee (FOMC) meeting, a surprisingly robust U.S. jobs report, and a landmark Supreme Court decision striking down the Administration’s use of emergency tariff authority under the International Emergency Economic Powers Act (IEEPA).

The combination of higher energy prices, sticky inflation expectations, and tightening financial conditions created a challenging environment for risk assets. Global equities faced broad headwinds, with U.S. markets pulling back from recent highs. The S&P 500 Index slipped 0.87% over the month, while the technology-heavy Nasdaq Composite fell 3.38%, led by weakness in Large Cap Growth. Meanwhile, the Federal Reserve opted to hold its benchmark interest rate steady amid the mounting uncertainty, acknowledging the complex crosscurrents of hot inflation, resilient labor markets, and geopolitical shocks.

Macroeconomic Review:

Economic indicators in March underscored a U.S. economy that continues to run hotter than anticipated, complicating the Federal Reserve’s policy path. The labor market demonstrated remarkable resilience; the U.S. economy added 178,000 jobs in March, nearly three times the market forecast of 60,000. The unemployment rate edged down to 4.3%, even as wage growth showed signs of moderating. This massive jobs beat reinforced expectations that the labor market remains historically tight despite higher borrowing costs.

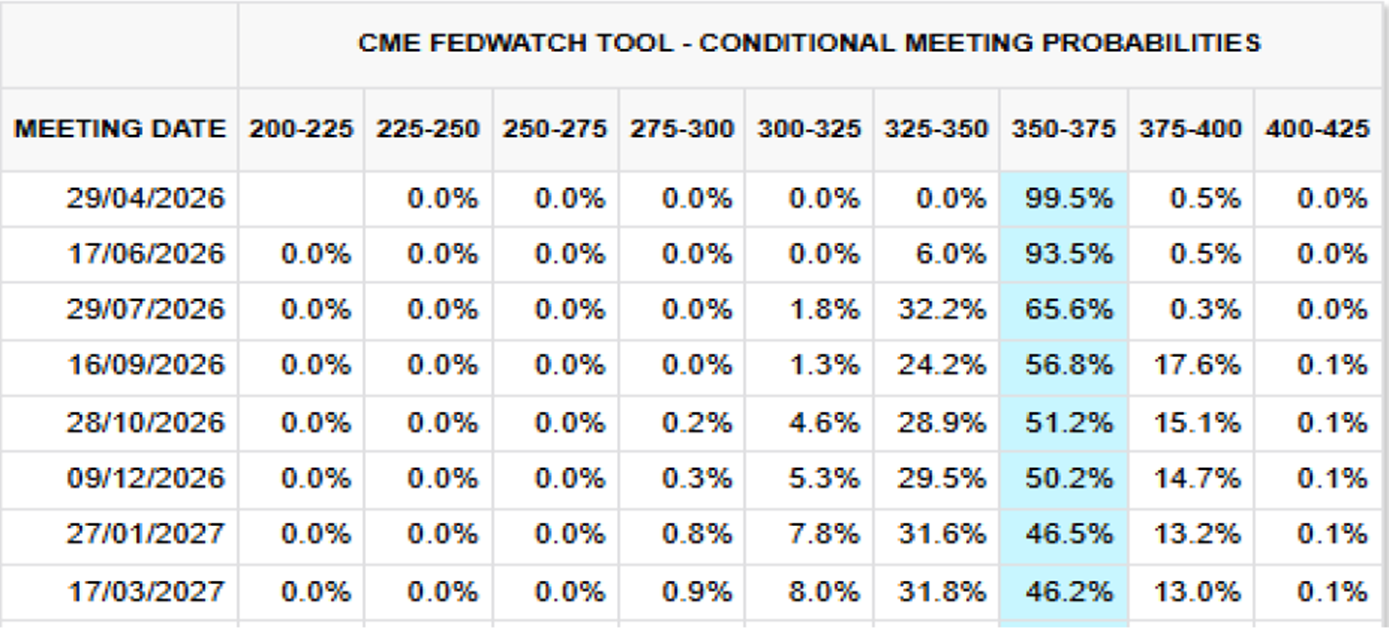

The Federal Reserve concluded its March 18 meeting by voting 11-1 to hold the federal funds rate steady in the 3.50% to 3.75% range. In his post-meeting press conference, Fed Chair Jerome Powell underscored the uncertainty surrounding the ongoing oil shock and admitted the U.S. had not made as much progress on inflation as policymakers had hoped. However, Powell firmly pushed back on the notion that the U.S. economy is experiencing “stagflation,” pointing to the robust labor data and underlying growth. The Fed’s favorite measures of inflation stayed hot early in the year, and the escalating Middle East conflict has now put the possibility of a Fed rate hike back on the table, further altering the timeline for any anticipated easing.

On the policy front, a major development occurred when the Supreme Court, in a 6-3 decision, struck down a key component of the Administration’s trade policy, ruling that the President does not have the authority under the IEEPA to impose sweeping reciprocal tariffs. This removed a central pillar of the current tariff framework and added another layer of complexity to the broader macro landscape.

Fixed Income:

U.S. Treasury yields rose significantly following the blowout jobs report and hawkish shifts in inflation expectations. The 10-year Treasury yield rose to 4.35% in shortened holiday trading at month-end, moving further away from the two-week lows reached earlier in March. Bond yields were driven higher by the realization that a strong labor market and surging energy prices will likely keep the Federal Reserve on the sidelines for an extended period.

Corporate credit markets also felt the strain of tighter financial conditions and a general risk-off sentiment. Sovereign bonds came under pressure globally, and investors began reassessing the premium required to hold long-duration assets in an environment where the Fed’s ability to offset supply-driven inflation shocks remains severely limited.

FOMC Rates Outlook Table:

Equity Markets:

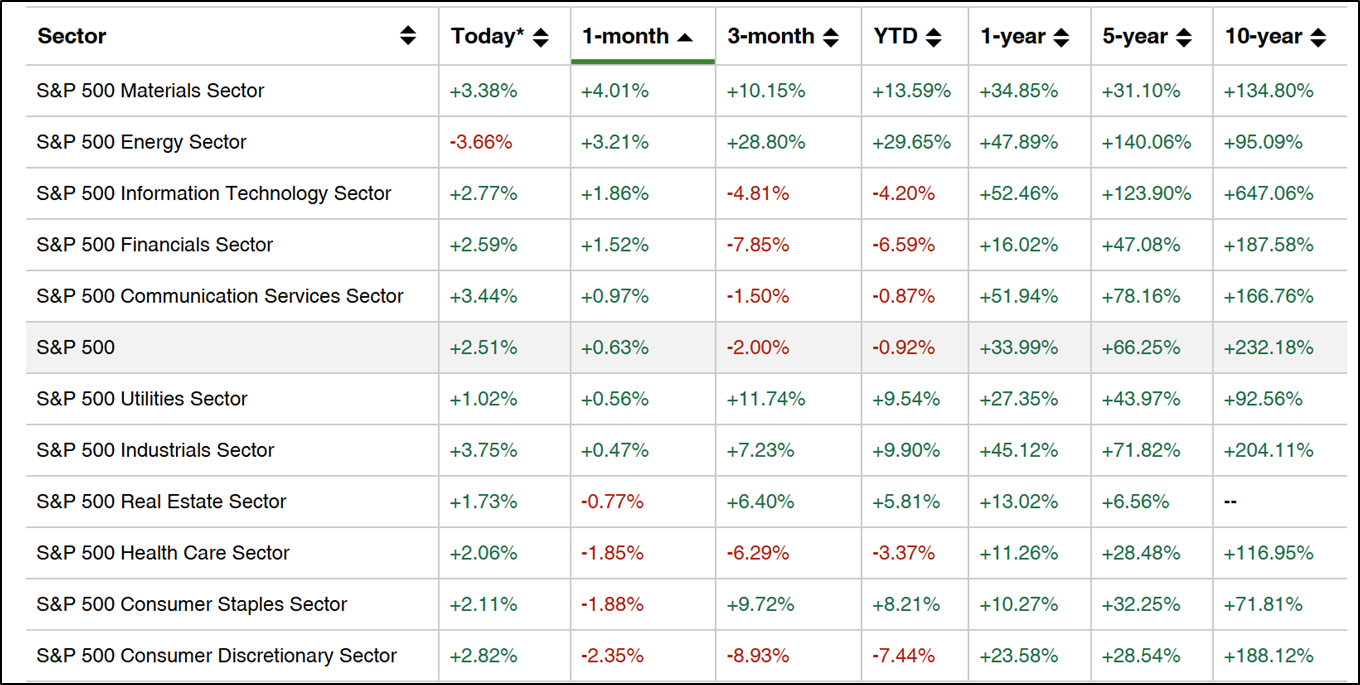

March halted the equity rally seen in earlier months. The S&P 500 lost 0.87%, while the Nasdaq Composite took a steeper hit, falling 3.38%. The sell-off was particularly pronounced in Large Cap Growth and technology-dominated sectors, which bore the brunt of the shifting rate expectations and elevated valuations.

Geopolitical risk forced a rapid reassessment among equity investors. Escalating rhetoric and infrastructure threats between the U.S. and Iran sent shockwaves through the market, ending the steady complacency that had characterized the winter months. Defensive sectors and energy producers saw pockets of strength, while software, logistics, and real estate faced sharp drawdowns amid fears of disruption and a higher-for-longer interest rate regime.

Monthly Sector Performance Like This:

Other Asset Classes:

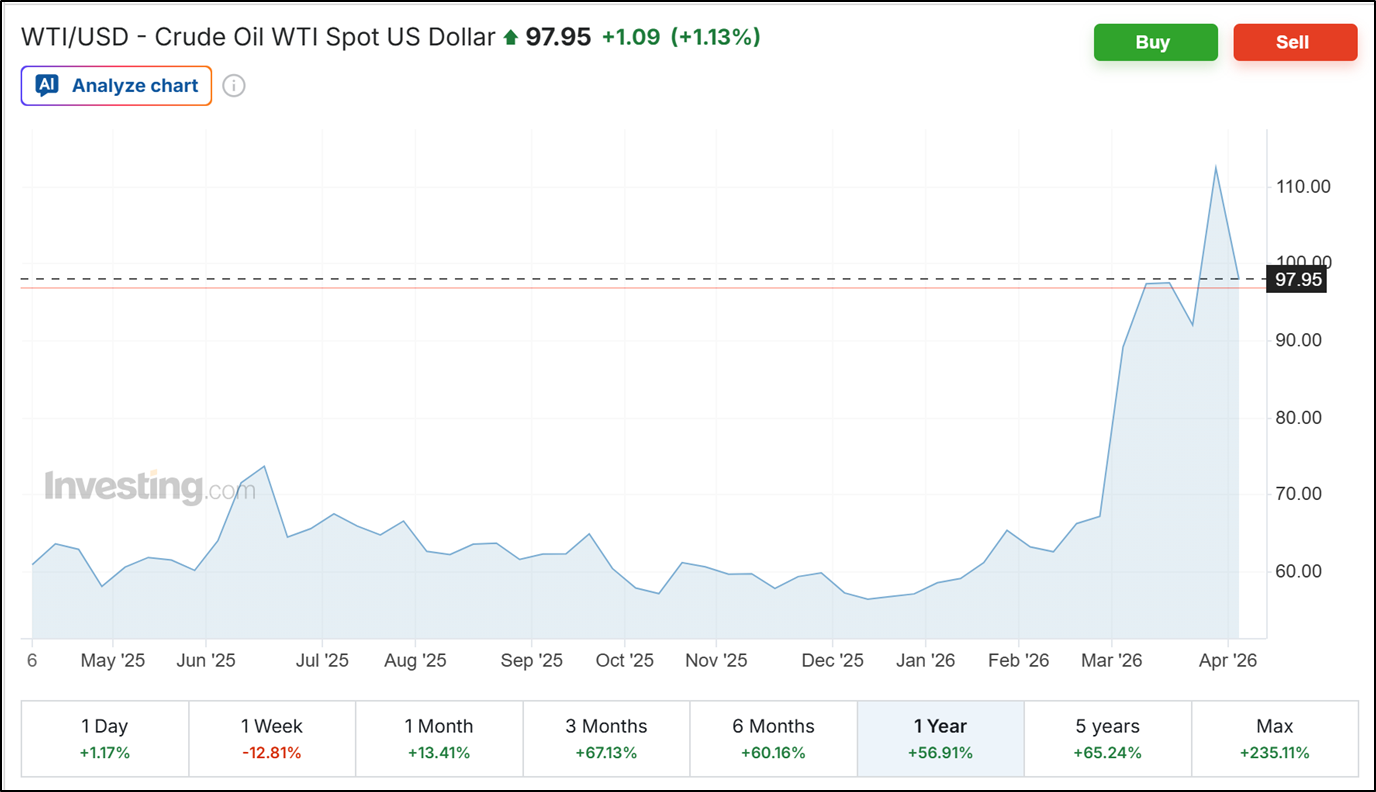

In commodity markets, energy prices surged dramatically. WTI and Brent crude spiked as the geopolitical conflict involving Iran threatened regional infrastructure and global supply chains. Conversely, precious metals exhibited unusual behavior: Gold did not act as a traditional safe-haven asset during the escalating conflict, reflecting the complicated dynamic where higher inflation expectations simultaneously reduced the likelihood of Fed rate cuts, strengthening real yields and pressuring non-yielding assets. Margin calls from levered investors added further pressure on Gold.

BRENT/WTI Graph:

As we enter the second quarter of 2026, evolving trade policy, geopolitical tensions, and a restrictive monetary environment shape a highly selective market landscape. The damage caused by inflation and energy shocks appears poised to dictate central bank actions for the foreseeable future. With global equities recalibrating to a reality where monetary policy has limited flexibility to rescue risk assets, the margin for error remains narrow.

Outlook:

As August progresses some of the uncertainty related to US trade policy should recede as more trade deals have been reached. The damage caused by tariff uncertainty appears to be less severe than initially anticipated. Market participants now seem to be more focussed on hard data in their investment decisions. No wonder we have seen the markets treading new heights with benign volatilities. Having said that, cracks seem to be appearing particularly with regard to labour market. Overall, the global economic momentum is likely to slow in the coming quarters. Also, with the huge rally in markets, equity valuations have become increasingly stretched even though the corporate earnings so far have been supportive. Investor sentiment appears to reflect an optimistic “Goldilocks” scenario—one in which growth accelerates, supported by fiscal stimulus and AI-driven productivity gains, while inflation remains contained. However, with global equities now trading at a price-to-earnings ratio of 20x, well above the historical average of 16x, the margin for error has narrowed significantly. In this context, diversification and selectivity remain paramount. Such positioning helps mitigate the twin risks of a potential inflation resurgence—leading to significantly higher bond yields—and the possibility of an economic slowdown or recession.

Cash

- The role of cash remains critical as a buffer in volatile markets, allowing portfolios to take advantage of pullbacks and market displacements as geopolitical events unfold.

Fixed income

- With the Fed battling sticky inflation and a surprisingly robust labor market, the risk of further rate volatility is high. Duration is best kept at medium-to-short levels. We prefer high-quality, intermediate credit which offers the best value on a risk-adjusted basis.

High-Yield will face further pressure with better buying opportunities down the line.

Equities

- With policy uncertainty now a permanent part of the 2026 investment playbook, investors must be nimble. Portfolios should be geared toward high-quality, cash-generative/high dividend, and conservatively capitalized businesses that can withstand higher input costs and borrowing rates.

Alternatives

- Private markets and carefully selected real assets can allow portfolios to benefit from sources of returns that are less directional and less correlated to the daily headline risks driving public markets.

A decline of Gold towards the $4,000 level could represent an attractive entry point.