Markets closed the first half of 2025 on a stronger footing, overcoming bouts of volatility along the way. Although geopolitical tensions and ongoing trade uncertainties triggered brief episodes of risk aversion, investor sentiment improved thanks to contained inflation in most regions and continued policy support. Trade dynamics remained a central market theme, following the 90-day tariff pause announced between the U.S. and China in May. Although this temporary truce provided a short-term boost to market optimism, questions surrounding its enforcement and the risk of renewed tensions sustained a backdrop of elevated volatility. Geopolitical risks escalated further in mid-June as the Iran-Israel conflict intensified, triggering a flight to safe-haven assets such as gold and U.S. Treasuries. Investors largely looked through the risks, although oil price volatility briefly rose due to concerns that a broadening of the conflict could have uneven impacts globally. Despite these headwinds, equity markets delivered solid returns, supported by encouraging developments in trade negotiations and continued enthusiasm around AI-driven innovation in the technology sector. Developed market equities extended their upward trend into June, with the MSCI World Index rising 4.5% for the month and 9.8% year-to-date, recovering from early-month disruptions related to the Israel-Iran conflict. Emerging markets also saw strong gains, with the MSCI EM Index gaining 6.1% in June and 15.5% year-to-date, driven by robust performance in China and renewed interest in risk assets. Macro factors like moderating inflation and continued strength in labour markets across the U.S. and Europe lent some support to investor sentiment while persistent uncertainty surrounding the future path of central bank policy, particularly from the U.S. Fed kept market participants cautious.

Macroeconomic Review:

In June 2025, global financial markets navigated a volatile landscape shaped by the interplay of macroeconomic uncertainty, shifting tariff policies, and escalating geopolitical tensions. The annual inflation rate in the US rose for the first time in four months, reaching 2.4% (annualized) in May 2025. This was a modest increase over the +2.3% rise in April but still one of the lowest prints over the past several years. The US economy contracted at an annualized rate of 0.5% in Q1 2025, a sharper decline than the second estimate of a 0.2% drop and the first quarterly contraction in three years. The weaker GDP figure was largely driven by significant downward revisions to consumer spending and exports. The University of Michigan’s consumer sentiment index for the US was revised higher to 60.7 in June 2025 from a preliminary of 60.5, compared to 52.2 in May. The unemployment rate, at 4.1 percent, changed little in June. The unemployment rate has remained in a narrow range of 4.0 percent to 4.2 percent since May 2024.

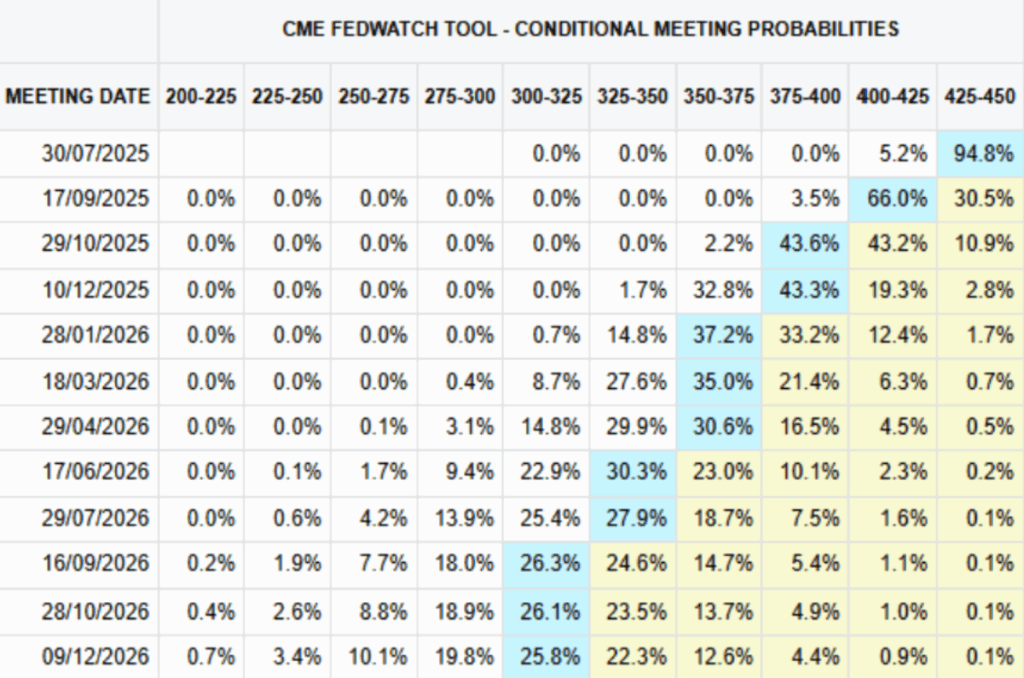

Against this backdrop, during its June meeting, the Federal Open Market Committee (FOMC) left interest rates unchanged at 4.25–4.50%, as policymakers take a cautious stance to fully evaluate the economic impact of President Trump’s policies, particularly those related to tariffs, immigration, and taxation. This marked the fourth straight meeting the Fed kept rates unchanged since cutting rates by 0.25% back in December 2024. The overall tone was cautious, reflecting persistent economic uncertainty and a desire to maintain policy flexibility while holding a positive view of the economy. The Federal Reserve remains caught between concerns over inflation and signs of economic weakness, such as declining small business and consumer confidence. Fed Chair Jerome Powell’s reluctance to forecast further rate cuts—and his repeated references to “uncertainty”—highlight the precariousness of the current landscape. The Fed also released updated economic forecasts, signaling expectations for higher inflation over the next two years and slower economic growth. Additionally, rate projections for 2025 and 2026 revealed growing divisions within the Fed’s Governing Council: some members favor a wait-and-see approach regarding the inflationary impact of tariffs, while others are more concerned about downside risks to growth.

Fixed Income:

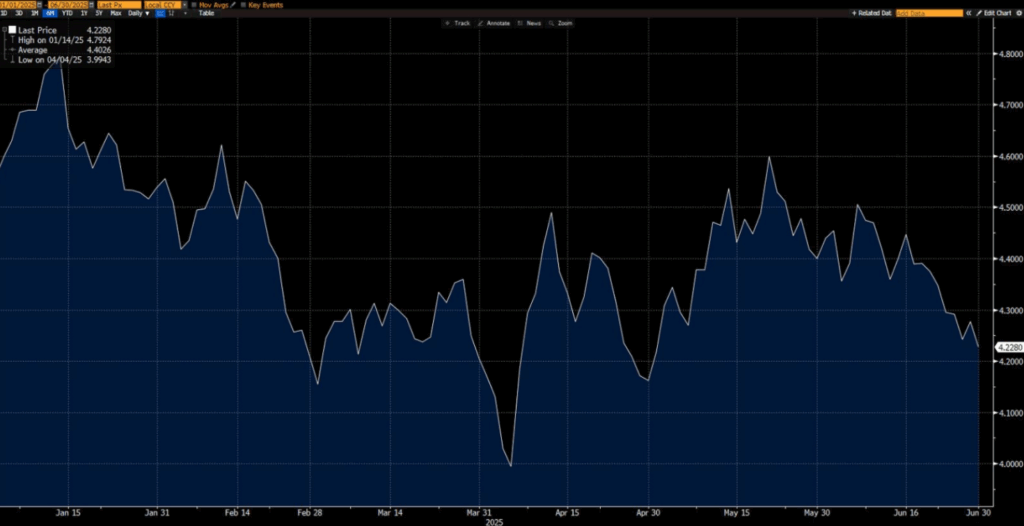

In June, global bond markets posted solid gains, supported by a decline in U.S. long-term interest rates and tighter credit spreads. US Treasury yields fell, boosting bond prices as investors sought safety amid geopolitical risks. The US Treasury yield curve bull steepened overall in Q2 – the 2s10s spread steepened by 18bp as the 2Y yield eased 16bp while the 10Y yield was up 2bp. Looking at the move through June alone, the curve shifted parallely lower by ~17bp. Overall, the Bloomberg U.S. Aggregate Bond Index returned +1.5% as the 10-year yield from from 4.41% to 4.24%. In contrast, European long-term yields edged higher.

In corporate credit markets, spreads continued to tighten, reversing the widening seen in April following the tariff announcements. U.S. high yield (HY) spreads narrowed to 292 basis points from a peak of 450 bps, while European HY spreads settled at 283 bps. Overall, HY spreads tightened by about 69 bps during the month. As a result, the U.S. HY index rose by 1.8%, significantly outperforming the European HY index, which gained just 0.2%. Among investment-grade bonds, top-rated U.S. corporates returned 1.9%, while their European counterparts posted a modest 0.2% gain. Investment grade led by AAA bonds and high-yield corporate bonds led by B rated bonds performed well during the review period.

Going forward, the US rate outlook will depend on the impact of tariffs, with its effect on prices and crucially inflation expectations, as well as economic activity. Market participants are pricing between 0-2 rate cuts of 25 bps each over the rest of the year depending on how the tariff and macro pendulum swings over the coming months. On the other hand, the interest rate outlook remains supportive in Europe. The ECB delivered its eighth rate cut of 25bps in June taking the key deposit rate to 2% and the BoE is expected to cut UK rates a further 2 times (25bps each) before the year end.

Equity Markets:

Most markets had a good June with the MSCI World Index rising by 4.5%, while the MSCI Emerging Markets Index advanced 6%. U.S. markets reached new all-time highs and outpaced European counterparts. This year has been nothing short of a wild ride for US equities. From dropping over 21% from its February peak to the lows seen in the second week of April to staging a V-shaped recovery, with the S&P 500 and Nasdaq 100 reaching new all-time highs – we have seen it all. Following a 6.3% gain in May, the S&P 500 added another 5.1% in June—marking the first back to-back monthly gains since September 2024. The combined 11.7% return for May and June was the strongest two month performance since December 2023. The Nasdaq Composite outperformed the S&P 500, rising around +6.6%, driven by notable strength in large-cap technology and AI-related stocks. The familiar mega-cap tech names reclaimed leadership in June, driven by their continued profitability and dominance in AI innovation and infrastructure. Yet they weren’t the only performers, industrials and financials also chipped in. Meanwhile, the health care sector was hit hard, dragged down by concerns over a proposed Republican budget bill. Small and mid-cap stocks bounced in June but still lagged their large-cap peers for the year. Nine out of the eleven large cap sectors ended YTD positive.

An interesting point to note with the market movement has been investor complacency, the VIX -the Volatility Index did not see much of a spike touching a highest level of only 22 and ending the month at yearly lows of 17, despite the ongoing tariff uncertainties and new Israel-Iran conflict. Last month, we observed how quickly markets had digested the unexpected tariff announcements from early April. June brought a similar pattern, with investors rapidly absorbing the shock of a U.S. military strike on Iran and largely brushing aside its implications. Investors largely looked through the risks, although oil price volatility briefly rose due to concerns that a broadening of the conflict could have uneven impacts globally.

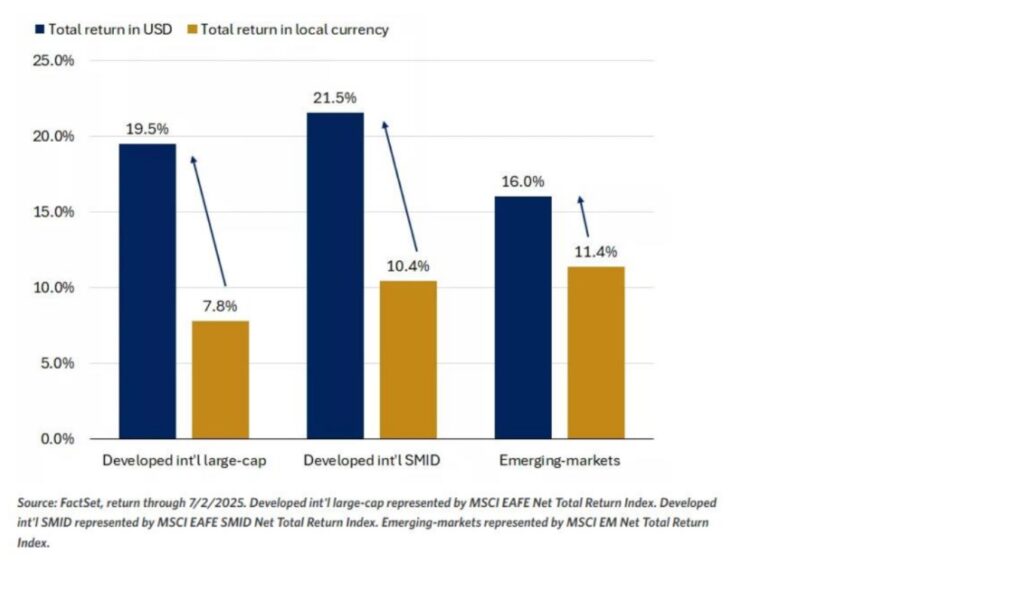

In other markets, the Stoxx Europe 600 fell by 1.3% (in euros), and the EuroStoxx 50 declined by 1.2%. Switzerland’s SPI (Swiss Performance Index) continued to underperform, dropping 1.9% (in CHF) while FTSE 100 edged up by +0.05%. Meanwhile, Japan’s Nikkei Index jumped 6.6% (in JPY) buoyed by a weaker U.S. dollar and shifting global sentiment. Emerging market equities outperformed their developed-market counterparts. Hong Kong’s Hang Seng Index (HSI) rose 3.4%, driven by a rebound in tech stocks. Other emerging markets saw varied performance based on their sensitivity to trade and tariff developments—South Korea’s KOSPI surged 13.9%, while India’s Nifty 50 gained 3.1%. For dollar-based investors, the diversification away from USD has rewarded investors not only by performance of the non-US assets but the huge forex gains on account of depreciating USD.

Other Asset Classes:

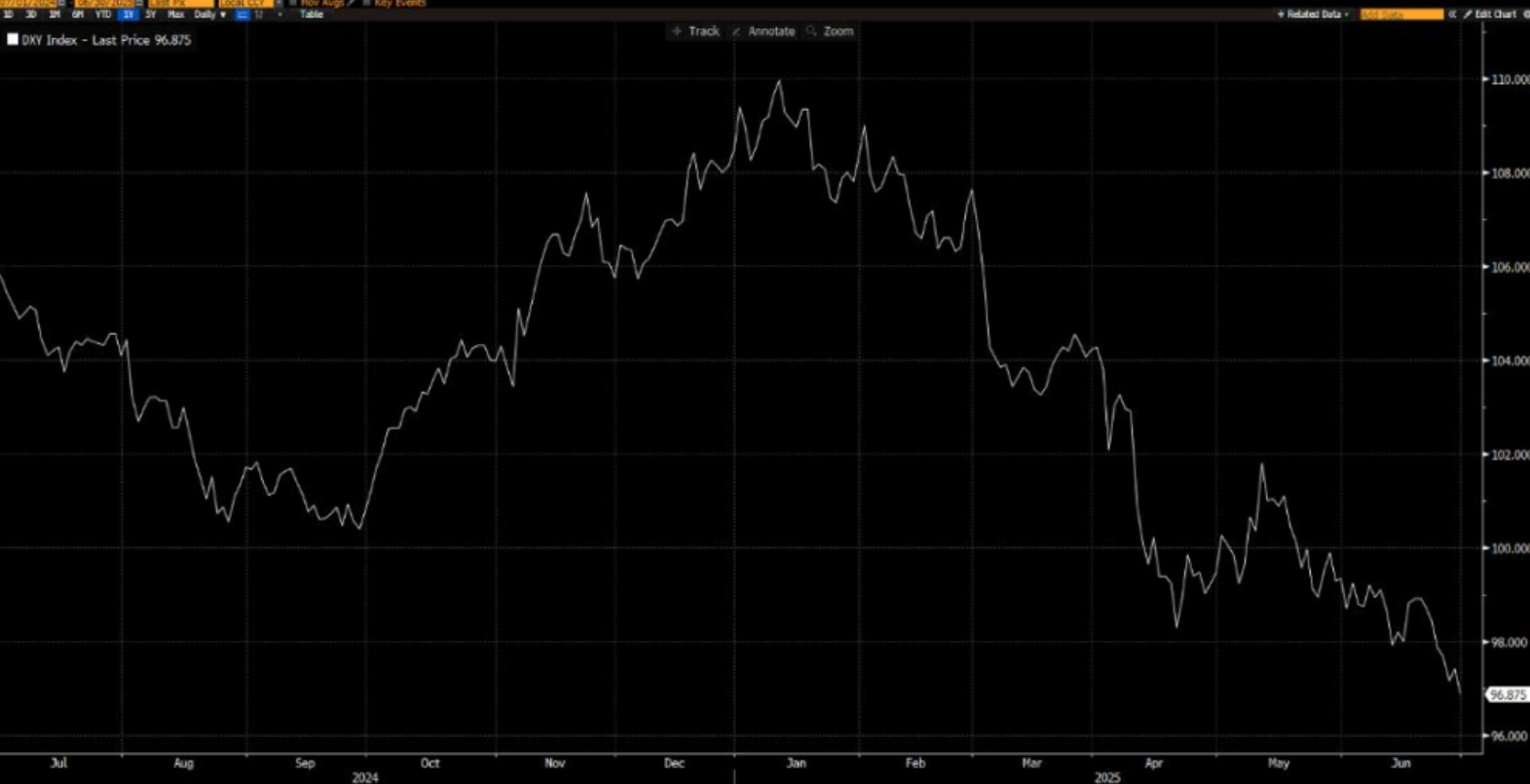

In June, the U.S. dollar continued its downward fall against most major currencies, reflecting renewed investor appetite for riskier assets alongside growing concerns over U.S. fiscal policy—particularly rising debt and deficits implications of President Trump’s “One Big Beautiful Bill Act.” Over the month, the dollar declined by 3.9% against the euro and 3.6% against the Swiss franc. The Japanese yen, however, was little changed, slipping just 0.1% against the dollar while the British pound appreciated by 1.97% against the greenback. The USD index, DXY, has reached 97 levels down over 10% since January when it had touched peaks of 110 levels. Gold prices also saw modest gains of +0.69 but failed to break new highs as economic and geopolitical uncertainty kept price movements muted. Commodity markets strengthened, with the Dow Jones Commodity Index rising by 2.69%, largely driven by a 6.4% increase in crude oil prices due to the escalating Iran-Israel conflict. The war between Iran and Israel caused significant geopolitical volatility, but its impact on broader markets was muted. The announcement of increased OPEC production also dragged on oil prices. Despite some short-term volatility prior to the US intervention on 22 June, which temporarily pushed Brent crude to an intra-day high of $80 a barrel, oil prices ultimately ended down at $68 a barrel.

Outlook:

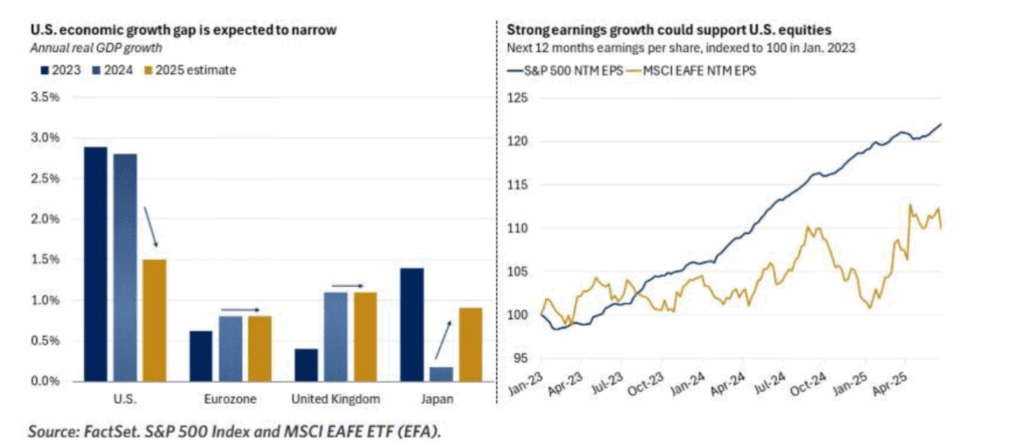

As we enter the second half of the year, we expect fundamentals and endogenous factors to regain the upper hand over geopolitics. While the growth outlooks of the major economic blocs differ, we do not expect recessionary outcomes as such, with macro variables remaining supportive. However, markets will continue to watch closely the global inflation, central bank policy moves and shifting geopolitical dynamics for any triggers. Also to be kept in mind is that -with market valuations running well above historical averages, the potential for downside volatility is rising— especially for the most richly priced stocks. Earnings season is approaching, and expectations have shifted. According to FactSet, the S&P 500 is now projected to report 5% year-over-year earnings growth for Q2 2025, down from the 9.4% forecast at the beginning of the quarter. Revenue growth estimates have also been revised lower, with Q2 sales expected to rise 4.2%, compared to an earlier projection of 4.7%. The S&P 500’s forward 12-month price to-earnings (P/E) ratio currently stands at 21.9, above its five- and ten-year averages of 19.9 and 18.4, respectively. As for the tariff negotiations, hopefully things will get cleared over the coming months, but it is still uncertain what the “other side of the decision” may be. No wonder all the Central Bank policy makers have kept the future decision path open and following a “wait and see” approach. It goes without saying that diversification and discipline remains of paramount importance in such times.

Cash

The role of cash becomes more important in volatile markets to take advantage of pull backs and market displacements.

Fixed income

With lot of day-to-day volatility, where rates markets are responding strongly to incoming data points—employment reports, inflation, GDP, tariff announcements, investors need to tread with caution.

As the Fed battles between its dual objective of inflation and employment in these uncertain times, the risk of direction and quantum of interest rate movement remains. Duration is best kept at medium levels. We prefer intermediate credit between 3-7 years, which offers best value on a risk adjusted basis.

In credit, the higher-quality segment is preferred, driven by what is considered to be better relative value. Investment Grade bonds still offer an attractive risk/reward profile. Income helps cushion the portfolio against steep pull backs.

In high yield, selection is key as credit spreads have potential to widen in case of unfavourable market scenario.

Equities

With policy uncertainty a part of the investment playbook investors should be nimble.

In line with the long-term investment philosophy, portfolios should be geared towards high-quality, cash-generative and conservatively capitalized businesses. Enthusiasm around AI-driven innovation in the technology sector is back on the forefront and should continue to boost portfolio returns.

Any market pullback can be seen as an opportunity to accumulate quality stocks for the long term.

Put selling strategies could be a good option to play market volatility opportunistically. • Diversification into Europe, China and India should help portfolios.

Alternatives

Price of Gold should continue to remain supported and provide diversification as uncertainties linger on with the communication chaos of the US Administration, while several Central Banks reduce their dollar exposure.

Private markets could allow portfolios to benefit from sources of returns that are less directional and less correlated than traditional asset classes.