July 2025 emerged as a month of resilience amid mounting uncertainties, with global equities edging higher despite geopolitical tensions and a complex policy landscape. The last week of July was particularly eventful with a rare convergence of market-moving events- we saw the July FOMC meeting, the US Treasury’s quarterly refunding announcement, key updates on trade negotiations ahead of the August 1 tariff deadline, critical US GDP and payroll data, and Q2 earnings from several of the “Magnificent 7” tech giants. The week spanned the full spectrum—from politics and central banks to macroeconomic indicators. Yet, the markets took everything in its stride ending the month at record highs. This month’s market rally pushed the S&P 500 and Nasdaq to new record highs, bouncing back from the post-Liberation Day selloff. The rally was fueled by easing tariffs and trade tensions, a strong start to the earnings season, and a resilient macroeconomic backdrop. Positive developments in the AI sector, increased deal activity, and the passage of the Big Beautiful Bill also helped boost market sentiment. Despite some concerns about rising interest rates, the market remained optimistic. Trade agreements played a significant role in the market’s performance, the U.S. finalized multiple trade deals, including agreements with the European Union and Japan. Negotiations with China also showed encouraging signs, with Treasury Secretary Bessent expressing optimism regarding the direction of discussions.

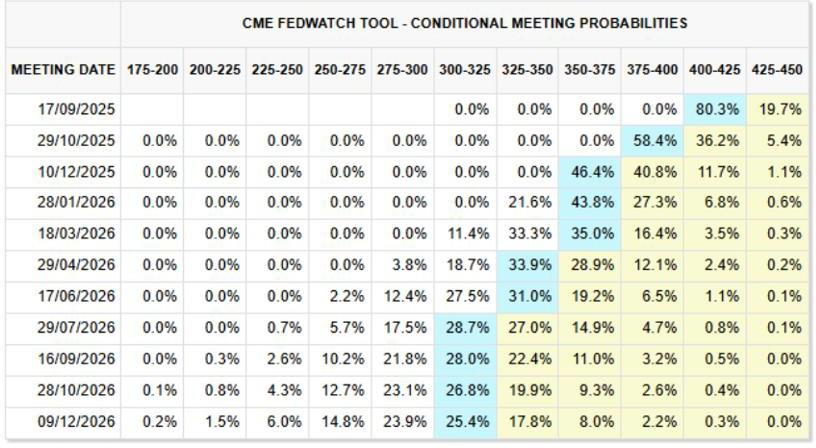

Over the month, global developed market equities rose 1.3%, marking a new all-time high. The S&P 500 rose 2.24% in July, extending its year-to-date gain to 8.58% and reached fresh all-time highs as strong Q2 earnings particularly from AI-driven technology giants like Microsoft and Meta overshadowed concerns about trade negotiations and hawkish central bank signals. During the month the Nasdaq gained 3.7%. The Federal Reserve concluded its July meeting keeping rates unchanged at 4.25-4.50%. However, the release of a weaker-than-anticipated July jobs report, alongside sharp downward revisions to May and June employment data shifted rate cut expectations. Bond markets are now fully pricing in 25bps rate cut in September, reflecting growing concerns of softening of the US economy. Amidst these expectations, treasury yields increased leading to a 1.5% fall in the global aggregate bond index. After months of negative performance, the USD appreciated in July contributing negatively to the aggregate returns.

Macroeconomic Review:

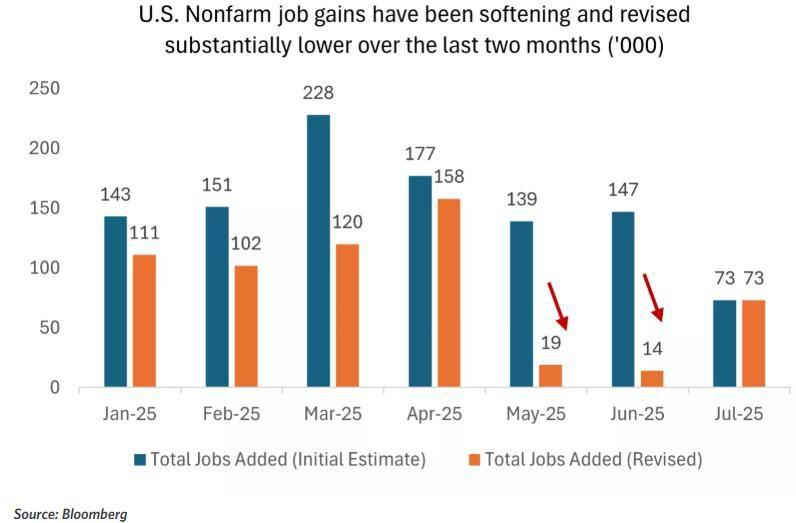

Economic indicators in July were kind of mixed. In terms of economic performance, US GDP rebounded sharply in the second quarter, expanding at an annualized rate of 3.0%, exceeding consensus expectations of 2.6%. This followed a 0.5% contraction in the first quarter. The strong rebound was largely driven by a historic 30% decline in imports, which contributed approximately five percentage points to overall growth. In contrast, domestic demand rose modestly by 1.2%. Consumer spending increased 1.4%, while business investment decelerated, residential investment contracted, and government expenditures declined. Labor market indicators in July reflected a cooling trend. Nonfarm payrolls rose by 73,000—the smallest gain since April, while the unemployment rate edged up to 4.2%. The labor force participation rate declined slightly to 62.2%. June inflation data showed the Consumer Price Index (CPI) rising 2.7% year-over-year and 0.2% month-over-month. Core CPI, which excludes food and energy, increased 2.9% annually. Food prices rose 3.0%, while energy prices declined by 0.8%. Despite mixed economic indicators, consumer confidence improved. The index rose from

95.2 in June to 97.2, reflecting easing concerns about the economic outlook and offsetting less favourable inflation and employment data.

The US Federal Reserve maintained its federal funds target range at 4.25% to 4.50%, citing ongoing inflationary pressures. However, the decision was not unanimous—Fed Governors Chris Waller and Michelle Bowman dissented, each favouring a 25-basis point rate cut. This marked the first dual dissent within the FOMC since 1993. The Fed acknowledged that economic activity had moderated, with the labor market remaining solid despite emerging signs of softening. Following the meeting, market expectations for rate cuts by year-end 2025 shifted to approximately 33 basis points, down from 43 basis points prior. In his post-meeting remarks, Fed Chair Jerome Powell emphasized that future policy decisions will remain data dependent. He outlined the criteria for the upcoming September meeting, highlighting the significance of headline unemployment and year-over-year core inflation. Although current data support continued policy stability, the softer-than- expected payroll report for July—along with downward revisions to May and June signals increasing vulnerabilities within the labor market and broader economy.

Fixed Income:

U.S. Treasury yields remained volatile throughout July. Early in the month, 10-year yields declined as investors adopted a risk-off stance ahead of the Federal Reserve meeting. However, yields rebounded following the announcement of a US -EU trade agreement, which strengthened the US dollar. By month-end, the 10-year yield hovered to around 4.40%. Since early April, the 10-year Treasury yield has traded within a 4.0% to 4.5% range, as investors continue to seek clarity on trade developments, monetary policy, and the broader economic outlook. Long-term yields outpaced short-term rates in July, driven by persistently elevated inflation, a longer-than-anticipated pause in Fed rate cuts, and increasing concerns over the

U.S. fiscal deficit. Sovereign bonds came under pressure due to this rise in long-term interest rates, while credit spreads tightened to new year-to-date lows, supported by improved visibility following tariff agreements and robust corporate earnings. Against this backdrop, the Bloomberg Global Aggregate Index posted a marginal decline of -0.1% in USD-hedged terms.

High-yield (HY) corporate bonds led performance across fixed income sectors in July. These securities benefited from reduced sensitivity to interest rate movements and relatively attractive yields. However, credit spreads—measuring the yield premium over comparable-maturity Treasuries—remain near 20-year lows, reflecting a heightened investor appetite for risk. The U.S. high yield (HY) spread narrowed to 278 basis points, down from a peak of 450 basis points in April. In Europe, HY spreads declined to 266 basis points. Over the month, high yield spreads compressed by approximately 30 basis points. The U.S. HY index rose by 0.5%, while the European HY index gained 1.1%.

With the geopolitical and policy uncertainty, major central banks have adopted cautious policy stances. The US Federal Reserve kept the federal funds rate between 4.25% and 4.50%, citing persistent inflation risks. The European Central Bank, which cut its key rate to 2% by June, signalled a pause in further easing. The Bank of Japan maintained its policy rate at 0.5%, while hinting at potential increases later this year.

Equity Markets:

July marked another strong month for equities, with the S&P 500 posting its third consecutive monthly gain and the Nasdaq extending its rally to a fourth straight month. The S&P 500 added 2.2% and racked up 10 record closing highs bringing its year-to-date gain to 8.58%. Notably, the S&P 500 experienced no daily moves of 1% or more in either direction—a level of stability not seen since July 2023. Market volatility remained subdued, with the VIX (Volatility Index) seeing subdued levels of 15. While Information technology was the top-performing sector, strength was also observed across several other sectors, including homebuilders, financials, automotive suppliers, and energy—particularly among major oil producers. In contrast, performance in logistics, entertainment, and media sectors lagged behind.

Second-quarter earnings reports provided a tailwind for equity markets. Q2 earnings season in the US is off to a strong start so far, close to 80% of companies in the S&P 500 that have reported thus far have beaten consensus earnings and revenue growth expectations, which is better than the long-term average. Eight of the sectors reporting year-over-year earnings growth, led by information technology, communication services, and financials. In aggregate, companies are reporting revenues that are 2.6% above the estimates, above both 5- and 10- year historical averages. Analysts now forecast 2025 S&P 500 earnings growth of 10.3%, up from the May 31 estimate of 8.8%. Strong earnings reports reinforced the view that the political turmoil of the past months has so far had only a muted impact on company earnings. The Magnificent Seven companies continued to report stronger earnings growth (17% vs. 4%) and revenue growth in technology outshone the rest of the market (14% vs. 7%), based on the companies that have reported so far. Large cap stocks outperformed small caps, 2.3% versus 1.9%. Large cap growth stocks outperformed value stocks, 3.1% versus 0.1%.

In other markets the MSCI EAFE Index, representing non-U.S. developed markets, fell 1.4% in July. European equities fell over the month on mixed corporate earnings reports and concerns over trade deals favouring the U.S. Emerging markets, represented by the MSCI Emerging Markets Index, rose 2.0%. The MSCI Asia ex Japan Index rose 2.6%, driven largely by stronger-than-expected economic data out of China. First-half GDP growth reached 5.3% year-over-year, surpassing the government’s 5% target. Industrial production also exceeded forecasts, rising 6.8% year-over-year in June. Additionally, the Caixin Manufacturing PMI climbed above the 50-point mark, indicating expansion in factory activity, although new export orders declined. Chinese equities were also supported by hopes of a trade deal between the U.S. and China. In contrast, European equities excluding the UK underperformed, with the regional index slipping 0.2%. Sentiment was weighed down by cautionary guidance from major continental technology firms, which cited potential negative impacts from evolving U.S. trade policy on their 2026 growth outlooks.

Other Asset Classes:

In other asset classes and currencies, the notable movers amongst others were the USD and Crypto currencies. The US Dollar which has faced persistent selling pressure throughout the year reaching lowest levels in 4 years, found support from the Federal Reserve’s relatively hawkish stance. The dollar strengthened to a two-month high against a basket of major currencies. It appreciated 3.2% against the euro, 2.4% against the Swiss franc, and 4.7% against the Japanese yen. On July 29, the U.S. Dollar Index surged by more than 1%—its strongest single-day gain this year—bringing its monthly increase to 3.1% as market participants priced out the “tariff risk premium.”

For the Crypto markets, the highlight was the passage of the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act), which was signed into law by President Trump on July 18. This landmark legislation establishes the first federal regulatory framework for payment stablecoins, introducing a two-tier licensing system. This renewed the interest in the crypto assets. Bitcoin rose 8.7% in July to end the month at $117,833.20, bringing the asset class up 27.2% YTD. However, Ethereum saw an even stellar surge of 52.1% to $3,807.42 as of July 31st, erasing the second- largest cryptocurrency’s YTD deficit to net a positive 13.3% gain through the first seven months of 2025.

Precious metals rallied in the first half of July but retraced much of their gains in the latter half. Gold prices declined by 0.40%, closing the month at $3,290 with a flat performance, although the metal remains up 25.35% year-to-date. Silver continued to narrow the performance gap with gold, with both metals ending the month in positive territory overall. Meanwhile, WTI crude oil rebounded sharply, rising 9.6% to close the month at $69 per barrel, supported by progress on global trade negotiations and President Trump’s threat of imposing tariffs on India for its continued purchases of Russian crude oil. These factors overshadowed a larger-than-expected production increase announced by OPEC+.

Ethereum price movement YTD – Source Bloomberg.

Outlook:

As August progresses some of the uncertainty related to US trade policy should recede as more trade deals have been reached. The damage caused by tariff uncertainty appears to be less severe than initially anticipated. Market participants now seem to be more focussed on hard data in their investment decisions. No wonder we have seen the markets treading new heights with benign volatilities. Having said that, cracks seem to be appearing particularly with regard to labour market. Overall, the global economic momentum is likely to slow in the coming quarters. Also, with the huge rally in markets, equity valuations have become increasingly stretched even though the corporate earnings so far have been supportive. Investor sentiment appears to reflect an optimistic “Goldilocks” scenario—one in which growth accelerates, supported by fiscal stimulus and AI-driven productivity gains, while inflation remains contained. However, with global equities now trading at a price-to-earnings ratio of 20x, well above the historical average of 16x, the margin for error has narrowed significantly. In this context, diversification and selectivity remain paramount. Such positioning helps mitigate the twin risks of a potential inflation resurgence—leading to significantly higher bond yields—and the possibility of an economic slowdown or recession.

Cash

The role of cash becomes more important in volatile markets to take advantage of pull backs and market displacements.

Fixed income

As the Fed battles between its dual objective of inflation and employment in these uncertain times, the risk of direction and quantum of interest rate movement remains. Duration is best kept at medium levels. We prefer intermediate credit between 3-7 years, which offers best value on a risk adjusted basis.

In the current times, where rates markets are responding strongly to incoming data duration can be added opportunistically at times of elevated yields while overall maintaining a medium duration profile.

In credit, the higher-quality segment is preferred, driven by what is considered to be better relative value. Investment Grade bonds still offer an attractive risk/reward profile. Income helps cushion the portfolio against steep pull backs.

In high yield, selection is key as credit spreads have potential to widen in case of unfavourable market scenario.

Equities

With policy uncertainty a part of the investment playbook, investors should be nimble.

In line with the long-term investment philosophy, portfolios should be geared towards high-quality, cash-generative and conservatively capitalized businesses. Enthusiasm around AI-driven innovation in the technology sector remains on the forefront and should continue to boost portfolio returns.

Any market pullback can be seen as an opportunity to accumulate quality stocks for the long term.

Put selling strategies could be a good option to play market volatility opportunistically.

Diversification outside of the USA into Europe, China should help portfolios.

Alternatives

Price of Gold should continue to remain supported and provide diversification as uncertainties linger on with the communication chaos of the US Administration, while several Central Banks reduce their dollar exposure.

Private markets could allow portfolios to benefit from sources of returns that are less directional and less correlated than traditional asset classes.