April 2026 delivered a powerful reversal from March’s risk-off sentiment, as markets staged a historic rally driven primarily by renewed optimism around artificial intelligence and a ceasefire announcement in the Iran conflict. The SCP 500 surged approximately 10.5%, while the Nasdaq Composite soared roughly 15.6%, both reaching new all-time highs. The rally was notably led by Technology / Semiconductor stocks, with the Philadelphia Semiconductor Index jumping nearly 40%. Emerging Markets outperformed dramatically as reflected in the MSCI Emerging Markets Index gaining 14.7%, powered by extraordinary gains in Taiwan (+26.2%) and South Korea (+38.2%). This marked a dramatic shift from March’s bearish dynamics, as geopolitical de-escalation and robust AI investment narratives reasserted investor confidence in Growth Equities.

However, inflation and energy pricing dynamics remained persistent headwinds throughout April. National average gasoline prices ended the month at $4.39 per gallon, up approximately 47% from $2.98 at the end of February as the Iran War has driven crude prices substantially higher, and for longer. While the ceasefire announcement provided relief, crude oil remained elevated at approximately $95-100 per barrel, contributing to inflation expectations that continued to weigh on fixed income. The 10-year Treasury yield rose modestly by roughly 5 basis points during April, as markets continued to price in sticky inflation risks surrounding energy disruptions. Despite the powerful Equity rally, Bond markets remained subdued, with the Bloomberg US Aggregate Bond Index posting mixed returns as higher yields offset gains from the brief risk-on phase.

Macroeconomic Review:

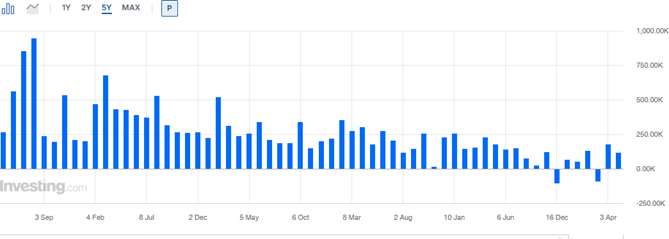

The US April jobs report provided a more mixed picture of labor market resilience. U.S. employers added 115,000 jobs in April, beating expectations of 55,000 jobs. This represented a sharp deceleration from March’s exceptional 178,000 job gain, suggesting that the labor market is normalizing after the earlier strength. The unemployment rate remained steady at 4.3%, while average hourly earnings growth showed signs of moderating, with monthly wage gains coming in at only 0.2% (versus the 0.3% forecast) and annual wage growth at 3.6% (below the 3.8% estimate). This moderation in wage pressure provided some relief for inflation-conscious policymakers, even as concerns about labor market softness emerged.

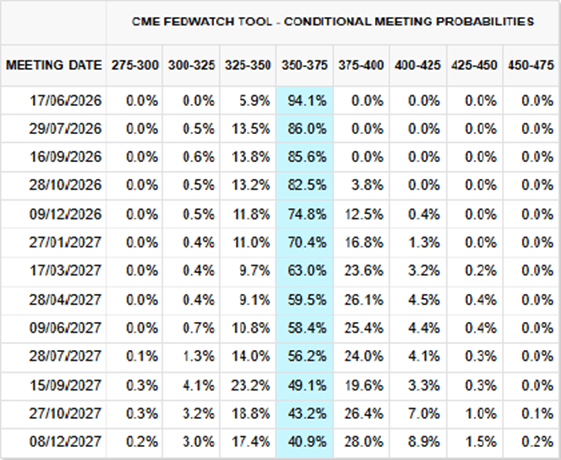

The Federal Reserve held its policy meeting in April, maintaining the Federal Funds Rate steady in the 3.50% to 3.75% range as inflation remained sticky and economic signals remained mixed. The softer jobs report and cooling wage growth provided some relief to inflation concerns, but energy prices and persistent supply-side shocks kept the possibility of future Fed action on the table. The expectations, reflected in interest rate futures, continue to suggest the Fed is likely to leave rates unchanged through 2026, though the inflation trajectory – particularly around energy costs – remains a key variable the Fed is monitoring closely. The central bank faces a delicate balancing act: supporting economic growth while remaining vigilant against resurging inflation driven by geopolitical supply shocks.

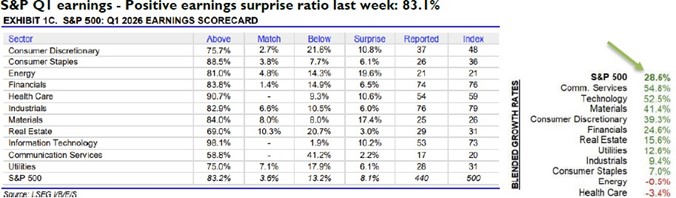

On the geopolitical front, a major turning point came with the ceasefire announcement between the U.S. and Iran, which immediately lifted risk sentiment and triggered a sharp reversal in commodity prices and equity rotation. This development removed a key risk premium that had been embedded in oil prices and volatility measures, allowing markets to refocus on fundamental drivers such as earnings growth and the artificial intelligence investment cycle. The ceasefire’s timing coincided with a robust earnings season, during which AI-related companies continued to deliver strong results, further fueling the market’s appetite for growth equities. In US, 83% of companies reported better than expected earnings.

US Non-Farm Payrolls Graph:

US Earnings Report:

Fixed Income:

U.S. Treasury yields rose modestly in April despite the rally in equities, as markets recalibrated duration expectations and inflation remained sticky. The 10-year Treasury yield ended near 4.37-4.40%, roughly 5 basis points higher than March month-end, reflecting ongoing concerns about the persistence of inflation in a higher-for-longer rate environment. Credit markets exhibited a dramatic risk-on reversal: high-yield bonds outperformed traditional investment-grade credit as investors embraced greater risk in search of yield. Investment-grade corporate spreads tightened meaningfully, and sovereign bonds benefited from the geopolitical de-escalation, though long-duration assets continued to face headwinds from elevated yields. Corporate credit markets also felt the strain of tighter financial conditions and a general risk-off sentiment. Sovereign bonds came under pressure globally, and investors began reassessing the premium required to hold long-duration assets in an environment where the Fed’s ability to offset supply-driven inflation shocks remains severely limited.

FOMC Rates Outlook Table:

Equity Markets:

April delivered one of the strongest equity rallies of 2026, reversing March’s losses and reaching new all-time highs across major indices. The SCP 500 gained approximately 10.5%, while the Nasdaq Composite soared roughly 15.6%, driven by a powerful rotation back into large-cap technology and AI-related companies. Growth equities, which had borne the brunt of March’s sell-off, captured approximately 12.4% in total returns versus just 7.2% for value strategies, signaling a decisive shift in investor sentiment toward companies leveraged to the artificial intelligence investment cycle.

PERFORMANCE OF VIX:

Geopolitical risk forced a rapid reassessment among equity investors. Escalating rhetoric and infrastructure threats between the U.S. and Iran sent shockwaves through the market, ending the steady complacency that had characterized the winter months. Defensive sectors and Energy producers saw pockets of strength, while Software, Logistics, and Real Estate faced sharp drawdowns amid fears of disruption and a higher-for-longer interest rate regime.

Monthly Sector Perfomance:

Other Asset Classes:

Commodity markets exhibited volatile price action in response to geopolitical developments and shifting energy demand expectations. WTI and Brent crude, which had spiked dramatically in March, receded moderately in April as the ceasefire announcement reduced supply-disruption fears. However, crude oil prices remained elevated at roughly $95-100 per barrel compared to pre-March levels near $67, reflecting persistent concerns about Middle East geopolitical stability and the structural impact of the earlier supply shock. Precious metals also reacted to risk-sentiment shifts: gold initially underperformed further in early April as real yields remained elevated and risk-off sentiment diminished, but it stabilized later in the month as some investors viewed the

$4,000-4,200 range as an attractive entry point given enduring inflation and geopolitical tail risks.

WTI Oil Price:

BRENT Crude Oil Price:

Gold Price:

Market Outlook & Positioning:

April’s powerful reversal showcases the acute sensitivity of modern markets to narrative shifts, geopolitical events, and momentum dynamics. As we head into May and the remainder of Q2 2026, three critical cross-currents will determine investment success: (1) the staying power of the AI rally beyond valuation-justified levels, (2) the trajectory of geopolitical risk and energy price stability, and (3) the Fed’s ability to thread a narrowing policy needle between supporting growth and combating sticky inflation. Markets are pricing in an extended pause from the Federal Reserve through year-end, but the inflation/energy nexus remains the variable that could force a reassessment. The narrow margin for error demands discipline, tactical positioning and a willingness to harvest gains when conviction wavers.

Cash:

The role of cash remains critical as a buffer in volatile markets, allowing portfolios to take advantage of pullbacks and market displacements as geopolitical events unfold.

Fixed income:

With the Fed keeps battling sticky inflation and robust labor market. We prefer high-quality, intermediate-duration credit: the 4.37–4.40% 10-Year Yield is reasonable, consider 5-8 year Treasury ladders or intermediate corporate credit to lock in carry while maintaining optionality for extension if growth falters. High-yield credit, while benefiting from April’s risk-on move, remains vulnerable to the next growth scare; investors should wait for wider spreads (400+ basis points) before building positions.

Equities:

With market uncertainty and valuations all near or at all-time-highs we reiterate our cautious stance and a preference to lock-in cash gains and replace exposure via Structured Products. Trim Mega-Cap Tech winners: take partial profits on positions up 20%+ since March lows and redeploy into Structured Products or undervalued quality compounders trading at 12-15x forward P/E with 5-7% Free Cash Flow yields.

Alternatives:

Diversification into private markets (Private Credit, Infrastructure, and Real Estate) is increasingly important given the unstable correlation between traditional stock-bond pairs. Private Credit at least at 9% offers both income and downside protection relative to public equities. Infrastructure assets (Toll Roads, Renewables, Utilities) provide inflation-linked cash flows and stable returns uncorrelated to Equity risk. Real Estate remains selective; avoid overvalued Office and Residential REIT positions but consider well-capitalized apartment and Industrial Logistics platforms. Hedge Fund strategies emphasizing Relative Value, Event-Driven opportunities, and Volatility harvesting may provide useful tail-risk protection given the elevated probability of dislocation.

Precious Metals & Commodities:

Gold remains a core portfolio hedge against inflation, currency debasement, and geopolitical tail risks. Levels near $4,100-4,150 would offer a reasonable entry point for 3-5% portfolio allocation while a pullback toward $4,000 would be attractive for accumulation. Oil markets remain range-bound at $90-105 per barrel given the Iran ceasefire, but investors should monitor further geopolitical developments; a breach above $110 would signal renewed supply concerns and warrant portfolio defensiveness. Avoid speculative positions in Industrial Metals as the global growth outlook is too uncertain and rate expectations too entrenched.