There are decades where nothing happens and there are weeks where decades happen. April has been one such month that has kept the world at the edge of the seat – what a roller coaster ride it’s been! Markets experienced significant volatility -the main driver being the on-again off-again Trump administration tariff impositions and the ensuing confusion over the end result in terms of both policy and impact. In normal times, it is macroeconomic data, such as the nonfarm payrolls, inflation data or purchasing managers’ index surveys that move markets. But we saw was a month that kept investors watching out for President Trump’s latest tweet with bated breath for potential market moves.

The month began with President Trump unveiling a broad and unexpectedly severe set of tariffs on 2nd April, the so called “Liberation Day”. This announcement triggered a sharp market sell-off and sent the VIX index—a measure of equity market volatility—soaring from 22 levels to 60, its highest level since the onset of the pandemic in 2020. However, markets regained ground later in the month after President Trump moderated the policy stance with a stunning U-turn: A 90-day delay was introduced for implementing reciprocal tariffs on countries that had not yet imposed retaliatory measures, and tariffs on various electronic goods were removed. Tensions between the U.S. and China also eased slightly as the administration adopted a more conciliatory tone. By month-end, developed market equities had risen 0.9%, though U.S. markets lagged behind their global counterparts. Growth stocks outperformed value stocks, with the latter weighed down by weak performance in the energy sector. The announcement on the Liberation Day also rattled bond markets alike. Yields on 10-year

U.S. Treasuries peaked at 4.6% on April 11 before easing to 4.2% by month-end. A fall in euro government bond yields contributed positively to the return of the global aggregate bond index. A stronger yen and euro versus the US dollar also helped to lift global bonds into positive territory in US dollar terms. Gold emerged as the main beneficiary of the heightened uncertainty, reaching a record high of $3,500 on April 22 while the other commodities lost ground with oil tumbling 16% amidst growing recession concerns and a decision from OPEC members to boost supply. Question on the potential erosion of the historic safe haven status enjoyed by the USD once again started doing the rounds.

Source: Bloomberg. Huge spike and subsequent stabilizing of the DXY, US 10Y and VIX index.

Macroeconomic Review:

On the macro front, while economic growth has slowed and sentiment has weakened, there are positive signs for the U.S. economy. The labor market remains robust and could be crucial for sustaining growth. Despite slower economic growth, unemployment claims have remained stable, and job creation continues at levels typically associated with economic expansion (+100k). March Job Growth Surpassed Expectations with the U.S. economy adding 228k new jobs, far exceeding the forecast of 140k and significantly improving on February’s 117k. This report provided temporary relief to investors, as many economists view the labor market as vital for ongoing economic growth. The April report, released on May 2nd, showed an additional 177k jobs, also surpassing the forecast of 133k. The unemployment rate remained steady at 4.2%. Retail Sales Rebounded in March with consumer spending rising by 1.4% in March, above the 1.2% forecast and significantly exceeding February’s 0.2% increase. While some economists anticipated a surge in

automotive sales due to pre-tariff purchases, retail sales excluding automobiles were also stronger than expected. CPI Inflation continued to ease for the 2nd consecutive month. Consumer prices increased by 2.4% (annualized) in March, coming in below the forecast of 2.6% and lower than February’s 2.8%. Core inflation, which excludes volatile food and energy prices, fell to 2.8%, the lowest rate since March 2021. Other indicators pointed to a slowdown in economic momentum—ISM Manufacturing fell into contraction at 49.0 while the ISM Services PMI declined to 50.8. Consumer sentiment fell for the fourth consecutive month in April, driven by concerns over the economic impact of tariffs and the potential return of high inflation.

Source: Bloomberg

Fixed Income:

The Bond markets saw significant volatility throughout the month, with Treasury yields spiking sharply even though it eventually settled lower. Bond Markets Benefited from Falling Yields -The Bloomberg U.S. Aggregate Bond Index gained 0.4% for the month, as the 10-year Treasury yield declined from 4.23% to 4.17%. The 10-year Treasury yield dropped by 0.20% following the tariff announcements on April 2nd, then surged by 0.50% over the next five days, before ending the month 0.06% lower. The sharp rate movement was attributed to several factors, including foreign central banks selling U.S. Treasuries, concerns over the growing U.S. budget deficit, and repositioning by hedge funds. Short-term rates remained stable as market expectations point to the Federal Reserve keeping rates unchanged at its May meeting. Interest rate futures indicate a 90% probability of no rate change during the Fed’s upcoming policy decision. However, the recent drop in the two-year yield suggests some investors anticipate the Fed may act more aggressively with rate cuts later in the year. The markets are now pricing 4 rate cuts by the Fed, with the Fed fund rate expected to be 3.4% by the end of 2025, compared with 4.1% at the start of the year and the Fed’s forecast of 3.9%. Credit spreads moved in line with shifts in risk sentiment throughout April, widening sharply following the tariff announcements but later recovering much of the lost ground. Higher-quality credit markets have remained relatively resilient despite recession concerns, likely due to the substantial improvements in corporate balance sheets seen in recent years. There seems to be a suggested shift in investor sentiment towards more “risk-off”, favouring lower-risk assets triggered by escalating trade tensions between the U.S. and China. While market participants were trying to gauge the fallout from the tariff dispute, sentiment was further dampened by reports/ “tweets” suggesting that President Donald Trump was considering removing Federal Reserve Chair Jerome Powell. However, concerns eased after Trump clarified that he had no such intention and hinted at a potential easing of tariffs on China.

US Equity Markets:

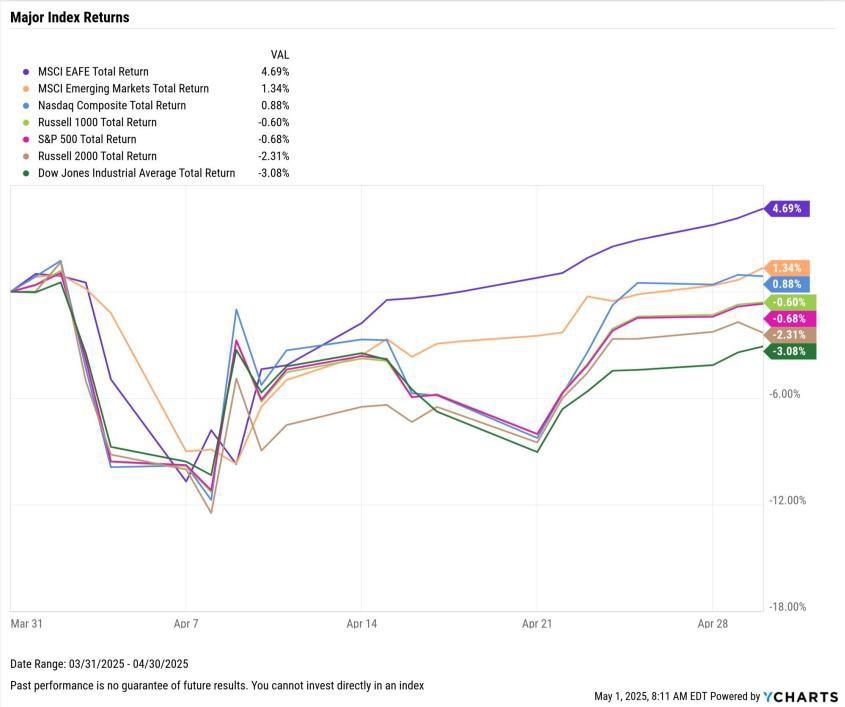

In April, mounting trade tensions created headwinds for U.S. equities, contributing to continued outperformance by international markets. Developed market equities (MSCI EAFE) rose 4.6%, outperforming emerging markets (MSCI EM), which gained 1.3%. The S&P 500 Index came close to entering bear market territory, falling 19% from its February 19th high through April 8th (a bear market is typically defined as a 20% decline). Concerns around U.S. trade policy, slowing economic growth, and rising inflation fears pressured the market with the market falling 11.2% from April 1–8, followed by an 11.8% rally from April 9 to month-end, driven by easing trade tensions and strong earnings from the big tech firms. Tech stocks posted a 1.6% gain in April, rebounding after the U.S. paused reciprocal tariffs on April 9. Positive earnings from Alphabet, along with better-than-expected results from Microsoft and Meta, fueled the sector’s recovery. Overall, the corporate earnings have provided some respite to the markets. Of the 180 S&P 500 companies that reported earnings, 73% exceeded analyst estimates—slightly below the five-year average of 75%. The biggest sector laggard was the Energy Sector that fell as oil prices tumbled. After all the interim volatile swings in the month, the large cap S&P 500 ended the month down a modest 0.7%, while small caps Russell 2000 fell 2.3%.

Other Major Markets:

Despite the tariff jolts over the month, the MSCI World Index rose by 0.7%. European equity markets declined, with the Stoxx 600 down 1.2% amid tariff concerns, while the S&P 500 slipped 0.8%. The Swiss Performance Index also retreated, down 1.9%. In contrast, Japan’s Nikkei gained 1.2%. Emerging market equities outpaced their developed counterparts by 1.0%. In China, the Hang Seng Index (HSI) tumbled 4.3%, while other emerging markets saw positive returns, including Brazil’s Bovespa (+3.7%) and South Korea’s Kospi (+3.5%).

In the eurozone, the flash composite PMI slipped to 50.1, reflecting a contraction in services activity (49.7), while the manufacturing index remained relatively steady at 48.7. This stability came despite the US imposing new tariffs—10% generally and 25% on autos—in early April. Lower energy prices and hopes for fiscal support helped offset some of the trade-related pressures. Nonetheless, eurozone consumer confidence declined further, underlining the impact of ongoing trade frictions and the unresolved war in Ukraine on sentiment. The European Union suspended retaliatory tariffs on steel and aluminium in an effort to create a more constructive environment for trade talks with the US. This move, alongside the formation of a new government in Germany, offered limited relief. However, European equities still posted a modest monthly decline of 0.4%. In the UK, April’s flash PMI data indicated weakening momentum, with the composite index falling into contraction territory at 48.2. The slowdown was attributed to a mix of global trade uncertainty and higher domestic taxes. UK equities declined by 0.2% over the period. In Japan, the all-industry flash PMI rose to 51.1, driven by a partial recovery in the services sector. However, the manufacturing PMI remained below the 50 mark, reflecting ongoing concerns about the adverse effects of US tariffs on Japan’s export-driven economy. Despite these challenges, Japanese equities rebounded from earlier weakness, gaining 0.3% in April and outperforming many peers. In the early part of the month, the US significantly raised tariffs on Chinese imports to 145%, prompting swift retaliatory measures from China. However, later signs of willingness from the US administration to enter negotiations, coupled with a strong first-quarter GDP reading of 5.4% year-on-year, helped boost investor sentiment and sparked a recovery in Chinese equities.

Other Asset Classes:

In other asset classes the biggest movers for April were the USD and Gold. The U.S. dollar continued to weaken against most major currencies, following a strong overall performance in 2024. After reaching a peak of 110 levels in Jan, the DXY Index corrected to 98 levels in April before recovering to 99+ levels by month end. Over the month, the USD declined by 4.7% against the euro and 6.6% against the Swiss franc, while the yen appreciated by 4.6% relative to the dollar. In commodities, gold reached a new all-time high of

$3500 on 22nd April ending 5.3% higher for the month. This surge was fueled by ongoing U.S. economic uncertainty and continuous gold purchases by world central banks looking to diversify away from dollar reserves. Meanwhile other metals and oil prices dropped sharply, with WTI falling 18% to $58 per barrel – the steepest drop since November 2021, primarily due to slowing demand from the U.S. and China, economic concerns, and rising supply from OPEC+ nations. Bitcoin on the other hand surprisingly moved largely like equities rising and falling with risk on/off sentiment respectively ending the month higher at $95000 levels.

Source: Bloomberg. Gold (XAU) price movement in 2025 (until 30.04.25)

Outlook:

Uncertainty around the direction of U.S. trade policy remains elevated and is expected to continue fuelling market volatility in the near term. In this context, diversifying equity exposure across regions can help reduce some of the risks linked to U.S. policy developments. While core government bonds experienced undue volatility in April, we continue to view high-quality fixed income as a strong hedge against recession risks. With inflationary pressures persisting, the role of alternative assets in shielding portfolios from inflation should not be overlooked. The Federal Reserve is set to meet in early May, while the market largely anticipates that the Fed will keep rates unchanged this month, with potential rate cuts postponed until June or beyond. Investors are closely watching for any signals about the FOMC’s stance on interest rates over the coming meetings. Corporate earnings results should likely be positive and continue to support markets. Uncertainty remains elevated and visibility is limited. That said, market sell-offs may be another opportunity to ‘buy the dip’, at least as long as recession fears in the US prove to be misplaced. Meanwhile, the surprise surge in credit spreads of late may be more of a blip, than a harbinger of a downturn. April’s market volatility serves as a reminder for investors to reflect—not to panic. Market cycles naturally include periods of uncertainty, but what helps investors endure them is clarity: understanding the purpose behind your investment approach and having confidence in the discipline that supports it.

Cash

The role of cash becomes more important in volatile markets to take advantage of pull backs and market displacements.

Fixed income

With lot of day-to-day volatility, where rates markets are responding strongly to incoming data points— employment reports, inflation, GDP, tariff announcements, investors need to tread with caution.

As the Fed battles between its dual objective of inflation and employment in these uncertain times, the risk of direction and quantum of interest rate movement remains. Duration is best kept at medium levels. We prefer intermediate credit between 3-7 years, which offers best value on a risk adjusted basis.

In credit, the higher-quality segment is preferred, driven by what is considered to be better relative value. Investment Grade bonds still offer an attractive risk/reward profile. Income helps cushion the portfolio against steep pull backs.

In high yield, selection is key. High-yield credit spreads have widened modestly in 2025 but have potential to widen more in case of unfavourable market scenario, as risk of stagflation/recession looms.

Equities

With policy uncertainty likely to persist for months, volatility in equity markets will remain at elevated levels.

In line with the long-term investment philosophy, portfolios should be geared towards high-quality, cash- generative and conservatively capitalized businesses. Focus on quality stocks, value and defensives.

Any market pullback can be seen as an opportunity to accumulate quality stocks for the long term.

Put selling strategies could be a good option to play market volatility opportunistically.

Alternatives

Price of Gold should continue to remain supported and provide diversification as uncertainties linger on with the communication chaos of the US Administration, while several Central Banks reduce their dollar exposure.

Private markets could allow portfolios to benefit from sources of returns that are less directional and less correlated than traditional asset classes. In particular, we like Private credit that provides access to a broad range of borrowers and sectors outside of public markets, adding diversification benefits. Since private loans are not actively traded, they are less exposed to daily market swings. Finally, a floating interest rate structure helps to make the asset class an effective hedge against inflation.