The old Wall Street adage-“Sell in May and go away” did not hold ground this time. Investors did quite the contrary and stayed invested and were duly rewarded. We saw a nice positive performance in May, with the S&P 500 rising about 6% (after falling nearly 6% in the first four months of the year). Since its April 8 lows, the S&P 500 has ascended over 18%. The strong market performance was largely fueled by a mid-month easing of U.S.-China trade tensions negotiations and a temporary postponement of planned tariff increases that helped alleviate recession concerns. The Q1 earnings results also continued to support the markets, leading to notable gains from the growth stocks, particularly the large tech. Despite these positive developments, market volatility remained high, particularly after President Trump floated the idea of imposing a 50% tariff on all EU imports—highlighting how swiftly market sentiment can shift in reaction to policy signals. Overall, developed market equities advanced 6.0% for the month. U.S. equities outperformed most global peers, with growth stocks (+8.7%) significantly outpacing value stocks (+3.2%). Small-cap equities also posted a strong recovery (+5.9%), buoyed by optimism that proposed tax and regulatory changes in the U.S. budget reconciliation bill would benefit smaller, pass-through businesses. Emerging markets delivered positive returns in U.S. dollar terms, supported by a weaker dollar. Global fixed income markets, on the other hand, declined, with the Bloomberg Global Aggregate Index down 0.4%. Mounting fiscal concerns in the U.S.—including Moody’s downgrade of the sovereign credit rating and weak demand for long-duration Treasury bonds—triggered a mid-month sell-off. However, bond markets partially recovered by month-end as easing trade tensions and receding inflation pressures helped restore investor confidence. Commodities underperformed, with the Bloomberg Commodities Index slipping 0.6%. Gold declined 0.8% amid improving risk appetite and reduced demand for safe haven assets. Oil prices rebounded with easing risk of recession.

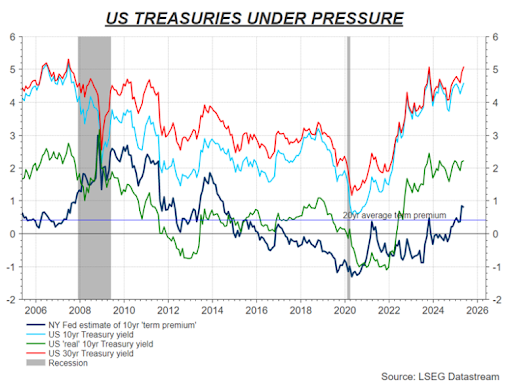

Chart: US Treasury Yield. Source LSEG Datastream

Macroeconomic Review:

Investor sentiment fluctuated as markets digested mixed economic data and shifting expectations around monetary policy. At its May 6–7 meeting, the Federal Reserve left interest rates unchanged at 4.25%–4.50%, maintaining a cautious tone in the face of what it termed “dual threats” — persistent inflation and a softening labor market. The meeting minutes, released on May 22, revealed that nearly all Federal Open Market Committee (FOMC) members were concerned about stalled progress on inflation. Simultaneously, early signs of weakening in the labor market began to emerge. Policymakers emphasized the high level of uncertainty surrounding the economic outlook, with several members warning of potential stagflation — a scenario in which trade-related disruptions could drive prices higher while simultaneously weighing on consumer demand.

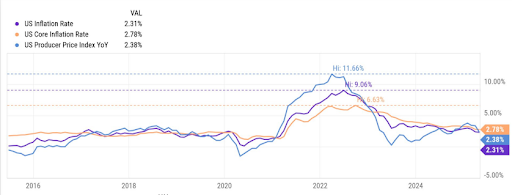

The stronger-than-expected Non-Farm Payrolls (NFP) report, which showed 177,000 jobs added—surpassing the forecasted 138,000 provided respite. The unemployment rate remained steady at 4.2%. Inflation showed further signs of cooling, with April’s headline CPI rising 2.3% year-over-year, below the anticipated 2.4%, while core CPI met expectations at 2.8%. Economic activity in both the manufacturing and services sectors also continued to improve. The monthly U.S. consumer confidence recorded a modest increase relative to an earlier preliminary reading, although it remained near the lowest level in almost three years following recently weak results. The University of Michigan’s Index of Consumer Sentiment rose to 52.2 from a preliminary figure of 50.8 released a couple of weeks earlier. May’s final figure was identical to April’s closing number.

Chart: US Inflation. Source Y Charts

Fixed Income:

Bond markets experienced heightened volatility in May, as investors navigated competing risks from persistent inflation, decelerating growth, and mounting fiscal concerns. Yields rose mid-month following the downgrade of the U.S. sovereign credit rating, which sparked a sell-off in longer-dated Treasuries and renewed scrutiny over the long-term sustainability of government debt levels. May saw interest rates rise as recession fears eased and the U.S. House of Representatives passed unfunded tax cuts. In May, the U.S. Treasury yield curve moved higher across the board, with yields rising roughly 25 basis points in a parallel shift from April. The yield on the 30-year U.S. Treasury bond soared above 5% mark, hitting its highest level since 2023, on worries about the long-term fiscal outlook of the US before ending the month at 4.91%. Yields on shorter-term Treasuries also declined, with the 10-year yield closing at 4.39% after having tested levels of 4.6.

Chart: Both US 30Y and 10Y rose in May with 30Y crossing 5%. Source Bloomberg

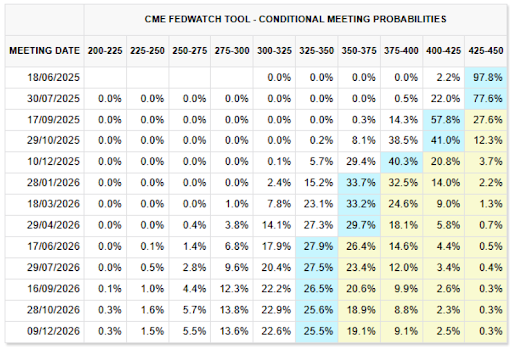

Against this landscape, the dollar-hedged Bloomberg Global Aggregate Index — the benchmark for investment grade bonds in developed markets — declined by 0.3%. The same index, hedged in euros, dropped by 0.5% over the same period. Bond markets in both Europe and the U.S. recorded negative returns, largely driven by an increase in long-term interest rates. Investor expectations have shifted, with the Federal Reserve now anticipated to make only two rate cuts this year, down from four projected a month earlier. The expected policy rate for December 2025 is now 3.8%, slightly lower than the 4.1% forecast at the beginning of the year. Markets also repriced rate cut expectations by the Fed following this and stable economic data from the US. From pricing in about 75bp in rate cuts for 2025 as of end-April, markets are now pricing-in about 50bp in cuts. In Europe, the European Central Bank delivered its seventh rate cut. Markets are pricing in two additional cuts by the end of 2025, with the year-end policy rate now expected at 1.7%, down from 1.9% at the beginning of the year.

US Equity Markets:

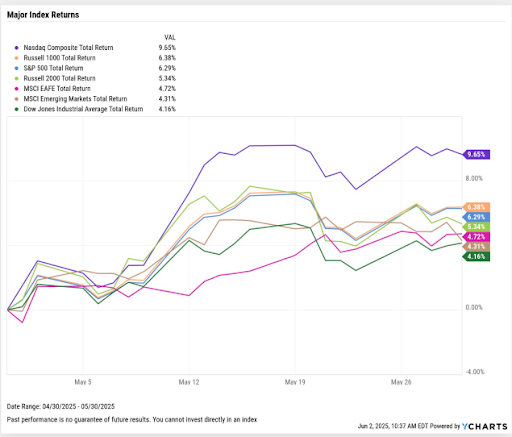

Following a turbulent and largely negative April, U.S. stock markets rebounded sharply in May. The easing of trade tensions between the U.S. and China served as a key catalyst, contributing to the strongest monthly performance for the S&P 500 and Nasdaq since November 2023. Large-cap tech stocks led the rally, with notable strength also seen in sectors like semiconductors, travel and leisure, automotive, and software. In contrast, areas such as managed care, pharmaceuticals, homebuilders, major oil companies, food and beverage, and telecommunications lagged. Information technology stocks were the primary drivers of this rally, with the S&P 500’s tech sector gaining over 10% for the month. The NASDAQ surged approximately 9.6%, while the S&P 500 advanced 6.2% and the Dow Jones Industrial Average rose 3.9%. Recent results have left the S&P 500, the NASDAQ, and the Dow little changed on a year-to-date basis, despite the market downturn from late February to early April.

The strong market performance was also supported by a solid first-quarter earnings season. With 97% of S&P 500 companies having reported, the blended year-over-year earnings growth rate reached 12.4%, marking the second straight quarter of double-digit growth for the index. Notably, 77% of companies delivered earnings that beat expectations, while 63% surpassed revenue forecasts. According to FactSet, companies in S&P 500 reported an average year-over-year earnings increase of 12.9% for the recently completed first-quarter earnings season. While this marks the second straight quarter of double-digit growth, it represents a slowdown from the 17.8% growth recorded in the previous quarter. Among the 11 sectors, healthcare led the way with a standout 43.0% earnings gain.

Other Major Markets:

In other markets European equities proved unexpectedly resilient in May, with the STOXX 600 rising 3% despite President Trump’s announcement of potential 50% tariffs on EU imports. After initial nervousness, progress in U.S.–EU trade negotiations helped ease recession concerns, while expectations for fiscal stimulus and upward revisions to earnings supported positive sentiment across the region. In contrast, the UK was the weakest performer among major equity markets, with the FTSE All-Share advancing 4.1% in May. Consumer staples, healthcare, and utilities underperformed. However, there were pockets of optimism: UK saw improvements in both retail sales and consumer sentiment, offering some support to the broader European outlook. Japanese equities on the other hand saw a strong rally, with the TOPIX Total Return rising 5.1% and the Nikkei 225 up 5.3%, largely driven by gains in large-cap stocks. Market sentiment improved on encouraging developments in U.S.– China trade talks, helping to ease recession concerns. Many Japanese companies released full-year results along with guidance for the fiscal year ending March 2026. While earnings projections remained cautious, there was a notable increase in shareholder returns through dividend hikes and share buybacks—highlighting ongoing corporate governance reforms and a focus on enhancing return on equity. Emerging market (EM) equities also advanced in May, although the MSCI EM Index trailed the MSCI World. The outlook improved following a temporary trade agreement between the U.S. and China, which reduced trade tension fears and helped ease concerns over a potential U.S. recession. Chinese equities benefited from tariff relaxation, with the Shanghai Composite up 0.8% for the week and the Hang Seng index in Hong Kong rising 2.1%. Initial optimism driven by the U.S.-China trade agreement, however, began to wane as an improved trade picture dampened expectations for further government stimulus. Analysts remain cautious, citing fragile domestic demand and external vulnerability. Momentum faded in the latter half of the month as focus shifted back to domestic economic headwinds. Retail sales growth slowed to 5.1% in April, down from 5.9% in March, and fixed asset investment increased just 4%, missing expectations. A sharp drop in property investment continued to drag on the broader economy, underscoring persistent structural challenges facing China’s recovery.

Other Asset Classes:

Commodities were the weakest performing asset class in May, with the broad Bloomberg Commodities Index declining by 0.6%. Gold rebounded to $3,289 but remained flat overall for the month, failing to break new highs as improving investor risk appetite reduced demand for safe-haven assets. The waning fear of recession on the other hand was supportive for industrial metals that rose 1.2%. Oil prices recovered, with WTI crude rising 5.5% to $61, following an 18% drop in April. The rebound was supported by a reduced perception of recession risk, though market attention remains on whether OPEC+1 will act on recent indications of a potential supply increase. May proved to be a good month amid regulatory progress, technological innovation, and rising institutional and governmental interest. Bitcoin rose 11% during the month, hitting a new all-time high of $112,000 on May 22. The rally was largely driven by increased demand from long-term institutional investors, including sovereign entities, local governments, and corporations, with retail investor activity playing a smaller role. Other digital assets also performed well with Ethereum surging 42%. In currencies, the U.S. dollar stabilized against most major currencies following a period of significant depreciation earlier in the year. However, it still posted modest declines, slipping 0.2% against the euro and 0.4% against the Swiss franc. The Japanese yen weakened further, falling 0.7% against the dollar.

Source: Bloomberg -1 Year USD chart (DXY Index)

Outlook:

May saw a somewhat return to normalcy with volatility receding and a notable shift back into risk assets. The easing of trade tensions contributed to a decline in recession concerns and a recovery in investor sentiment. However, with inflation remaining elevated and fiscal pressures intensifying, the macroeconomic outlook remains delicately balanced. Navigating the global economy and managing capital market volatility has always posed challenges, but the uncertainties emanating from Washington makes this task even more difficult. Despite the ongoing tariff back-and-forth, the key takeaway is that uncertainty persists, requiring investors to remain patient as markets await a more stable and coherent trade policy framework. Greater clarity may potentially emerge around key upcoming dates—July 9, marking the end of the 90-day suspension on tariff rate adjustments, and August 12, when the pause in tariff measures with China is set to expire. In this context, we continue to emphasize the importance of maintaining a well-diversified portfolio capable of withstanding two-sided risks: persistent inflation on the one hand and the possibility of slowing growth on the other. The US is on a path of slower, still good, but no longer ‘exceptional’ growth. Given more attractive valuations and supportive policy dynamics in other regions, diversifying into other regional equity markets may help portfolios. In an environment of heightened market volatility, diversification and selectivity remain critical. As we have seen over the course of this year, market narratives can shift more rapidly than most investors can reposition their portfolios. Rather than reacting to the latest trends or short-term concerns, a more prudent approach is to maintain discipline and a long-term perspective. Investors should consider expanding their exposure across geographies, sectors, and asset classes. Given the current high level of policy uncertainty, avoiding extreme positions and adopting a balanced, middle-of-the-road strategy appears to be a sensible course of action, regardless of the potential twists and turns ahead.

Cash

• The role of cash becomes more important in volatile markets to take advantage of pull backs and market displacements.

Fixed income

• With lot of day-to-day volatility, where rates markets are responding strongly to incoming data points— employment reports, inflation, GDP, tariff announcements, investors need to tread with caution.

• As the Fed battles between its dual objective of inflation and employment in these uncertain times, the risk of direction and quantum of interest rate movementremains. Duration is best kept at medium levels. We prefer intermediate credit between 3-7 years, which offers best value on a risk adjusted basis.

• In credit, the higher-quality segment is preferred, driven by what is considered to be better relative value. Investment Grade bonds still offer an attractive risk/reward profile. Income helps cushion the portfolio against steep pull backs.

• In high yield, selection is key. High-yield credit spreads have widened modestly in 2025 but have potential to widen more in case of unfavourable market scenario.

Equities

• With policy uncertainty likely to persist for months, volatility in equity markets will remain at elevated levels.

• In line with the long-term investment philosophy, portfolios should be geared towards high-quality, cash generative and conservatively capitalized businesses.

• Any market pullback can be seen as an opportunity to accumulate quality stocks for the long term.

• Put selling strategies could be a good option to play market volatility opportunistically.

• Diversification into Europe,

Alternatives

Price of Gold should continue to remain supported and provide diversification as uncertainties linger on with the communication chaos of the US Administration, while several Central Banks reduce their dollar exposure.

• Private markets could allow portfolios to benefit from sources of returns that are less directional and less correlated than traditional asset classes. In particular, we like Private credit that provides access to a broad range of borrowers and sectors outside of public markets, adding diversification benefits. Since private loans are not actively traded, they are less exposed to daily market swings. Finally, a floating interest rate structure helps to make the asset class an effective hedge against inflation.